The Greek debt crisis is back in the news. According to the Greek authorities, the country’s economy shrank by 0.4 per cent in the final quarter of 2016. “Experts” had expected it to grow by 0.4 per cent.

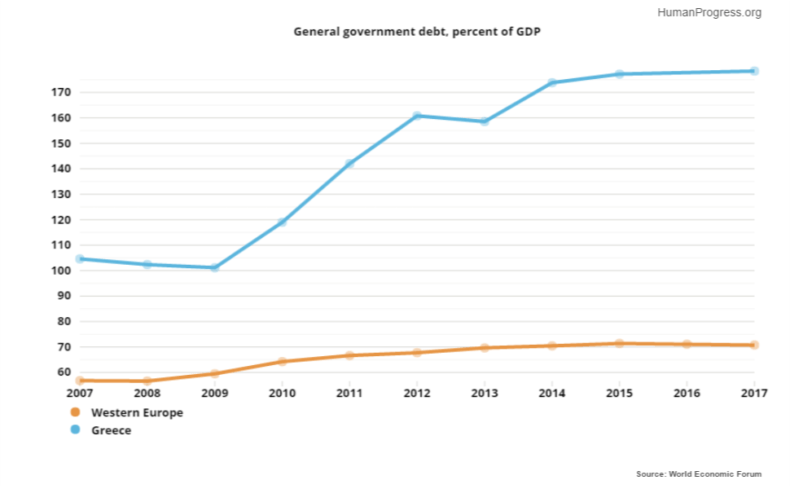

Despite a number of bailouts amounting to some 240 billion euros, and a host of supposed reforms (which I will address below), the Greek economy is refusing to grow. As a consequence, debt has ballooned to around 180 per cent of gross domestic product.

Jeroen Dijsselbloem, the head of the Eurogroup of finance ministers, has downplayed the disappointing data out of Athens, saying that the Greek situation is not an “acute crisis.” That was to be expected, of course.

The eurozone authorities have made it clear that they will do anything in order to keep Greece in the common monetary area. If one country dumps the euro, after all, others might soon follow.

But to paraphrase Emperor Hirohito upon surrendering Japan to the Americans at the end of World War II, “the common currency has developed not necessarily to Europe’s advantage”.

The International Monetary Fund, which has collaborated with Frankfurt and Brussels to bail out the Greeks on previous occasions, seems to be having doubts about continuing with a policy that is yet to yield positive results.

A week ago, the IMF stated that the Greek debt is on an “explosive” (i.e., unsustainable) path. That is a problem for at least two reasons. First, a number of Greece’s creditors, including Germany and Finland, are legally obliged to withdraw from the latest €86 billion rescue package if the IMF ends its support for the government in Athens.

Second, Donald Trump appears not to be a big fan of the European Union and its obsession with ever deeper integration – the poster child of which is the misbegotten single currency. He may yet instruct the US representative at the IMF to join Asian and Latin American countries in preventing the Europeans from continuing to use the IMF as their regional piggy bank.

Of course, as my Cato Institute colleague Ian Vasquez has noted in the context of Western aid to developing regions (e.g. sub-Saharan Africa), aid agencies, like the IMF, do not like to stop lending money. As he says:

“They are in the awkward position of trying to discourage bad policy and encourage policy change through loan cut-offs and, at the same time, trying to encourage policy change through the release of more aid if a country promises such change.

“Releasing that aid would once again jeopardise reforms. Not releasing that aid, on the other hand, would mean that policy change would occur without aid and thus run the risk that the agencies would be viewed as irrelevant.

“From an institutional perspective, lending agencies simply cannot afford to let … countries reform on their own. Both the aid institutions and the recipient governments know this, thus further reducing the credibility of so-called conditionality.”

Speaking of reforms, the logic behind the Greek bailouts was as follows. The international community would lend Greece money in return for deep economic and administrative reforms that would, in turn, set the Hellenic Republic on a path to sustained high rates of growth. As the Greek economy grew, the hope was that its sovereign debt would be paid off.

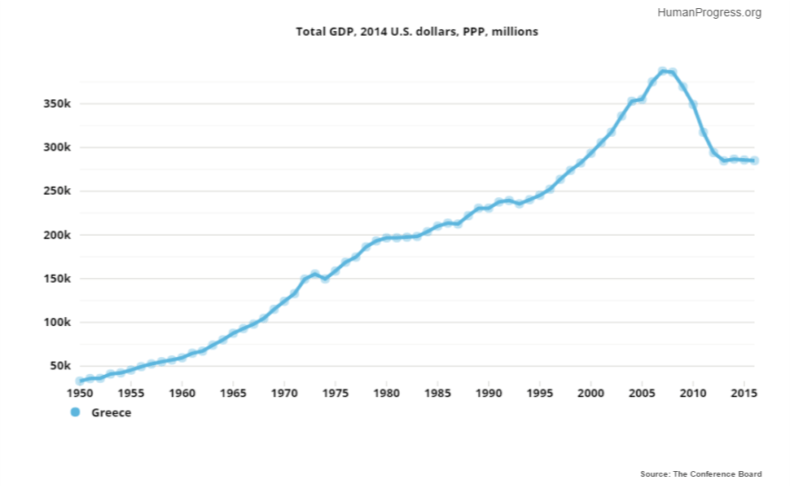

Unfortunately, the size of the Greek economy is where it was, roughly speaking, in 1999. Sustained and rapid growth, in other words, remains elusive.

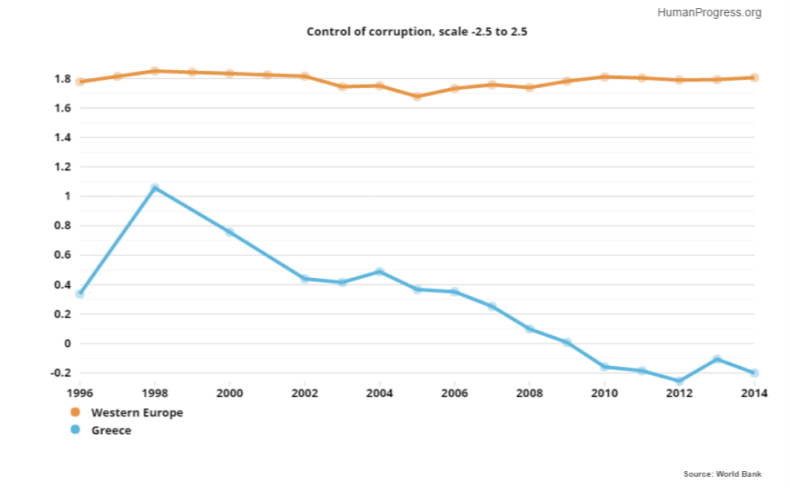

Part of the reason for that sorry state of affairs is that Greece has not reformed itself and remains stuck in its typically Byzantine way of doing things. Don’t take my word for it: consider data collected by the World Bank.

According to the Bank, control of corruption in Greece was worse in 2016 than when the Great Recession started.

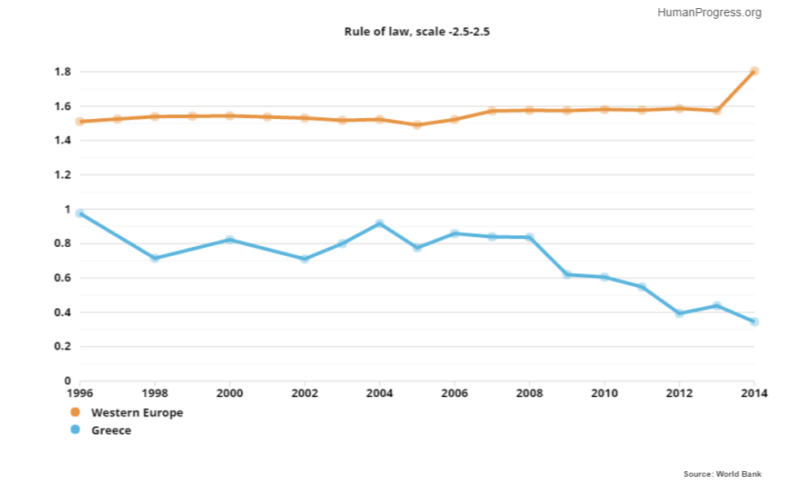

The rule of law, the Bank continues, has substantially deteriorated in the aftermath of the debt crisis.

The rule of law, the Bank continues, has substantially deteriorated in the aftermath of the debt crisis.

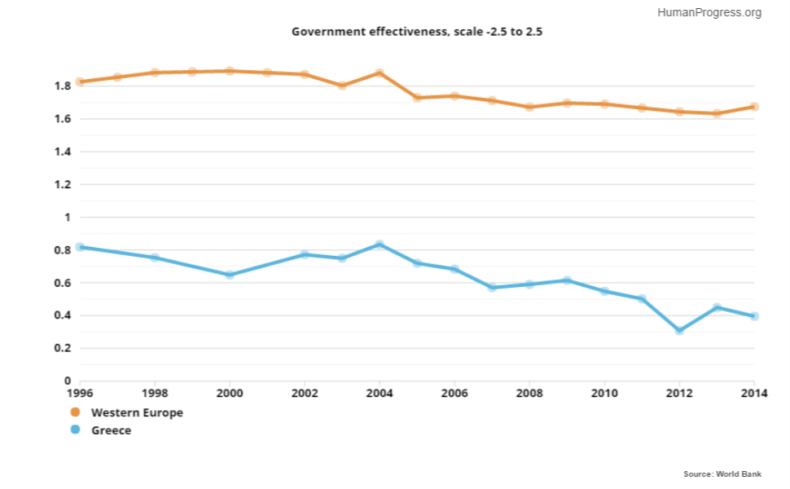

In the same vein, government effectiveness (a measure that captures perceptions of the quality of public services, the quality of the civil service and the degree of its independence from political pressures, the quality of policy formulation and implementation, and the credibility of the government’s commitment to such policies) has also declined.

In the same vein, government effectiveness (a measure that captures perceptions of the quality of public services, the quality of the civil service and the degree of its independence from political pressures, the quality of policy formulation and implementation, and the credibility of the government’s commitment to such policies) has also declined.

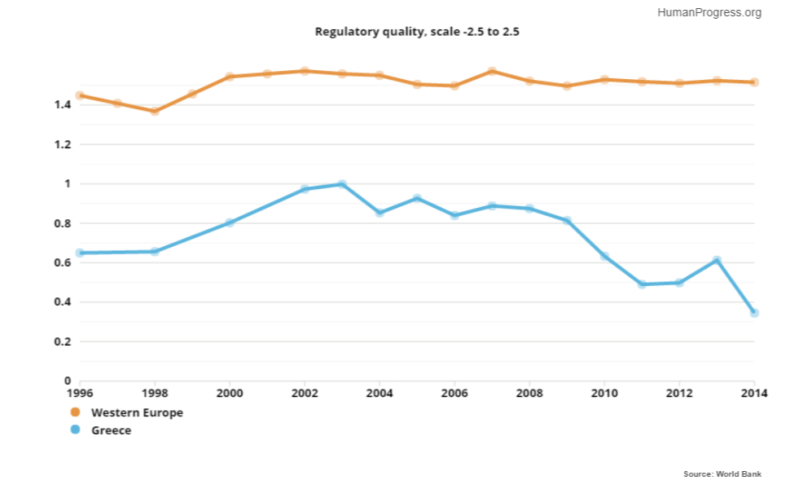

The same is true of regulatory quality.

The same is true of regulatory quality.

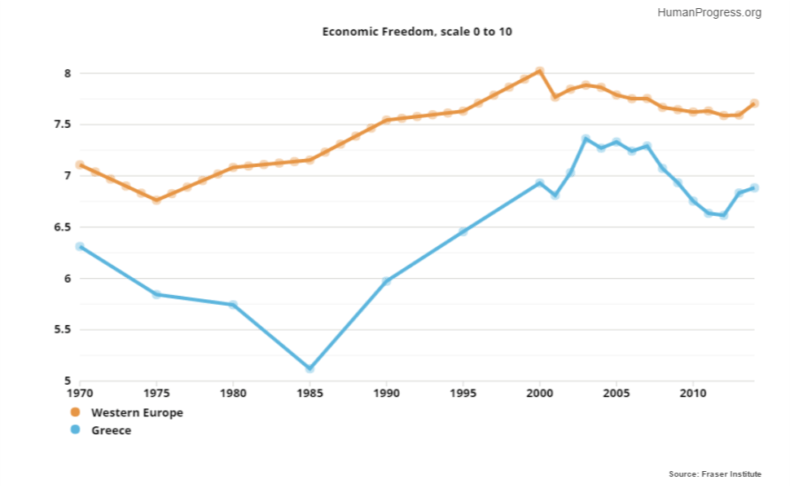

Last, but not least, overall economic freedom in Greece is lower than it was at the start of its recent economic troubles.

Last, but not least, overall economic freedom in Greece is lower than it was at the start of its recent economic troubles.

Just about the only bright spot on the horizon is that it is slightly easier to do business in Greece than it used to be before the crisis. Unfortunately, relatively few people will be tempted to start a business in a country, as thoroughly dysfunctional as the World Bank shows Greece to be.

Is it any wonder, therefore, that the Greek economy is stagnating and its debt growing? The IMF, along with its European allies, has failed to induce Greece to reform. They ought to stop throwing good money after bad and allow Greece to default.