The White House has announced that it will impose a 10 per cent tariff on imported aluminium and 25 per cent on imported steel. Few details are available. Apparently, these tariffs are being imposed under Section 232 of the Trade Expansion Act of 1962, which gives the president authority to restrict imports and impose limited tariffs if the Department of Commerce concludes that the current reliance on select imports is a national security threat. Whatever the reason, imposition of these tariffs is bad economic policy and its timing is inopportune.

The economic effects of these tariffs on the macroeconomic environment will depend critically on whether they damage business and household confidence. If confidence is unaffected, the economic effect would be relatively small in the aggregate, although it would harm some industries more than others. In 2017, the US imported 34 million metric tons of steel with an import value of $29 billion and 6 million metric tons of aluminium with an estimated import value of $16 billion. Multiply these amounts times the proposed tariffs, and the new import fees are very small relative to the $2.4 trillion of total US imported goods.

However, the danger is if these tariffs adversely jar confidence — perhaps fueled by foreign retaliation — heightened uncertainties would lead businesses to tone back their expansion plans and the trajectory of consumer spending would be softer. The negative effect could be material. A deceleration in US and global trade flows would be a negative. These negative effects would mitigate, but unlikely sufficiently large enough to negate, the positive impacts of the Tax Cuts and Jobs Act.

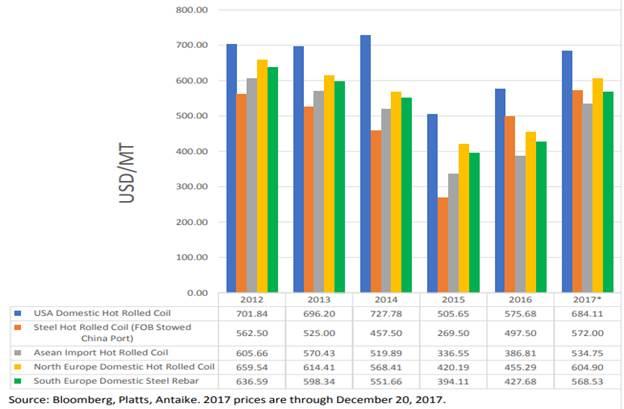

According to data in the US Department of Commerce’s report, The Effect of Imports on the National Security, published on January 11 2018, the United States currently produces 82 million metric tons of steel and its productive capacity of 113 million metric tons is sufficient to meet domestic demand. The United States produces 785,000 metric tons of aluminium, but its productive capacity is insufficient to meet demand. However, the report shows that US-sourced steel products are significantly more expensive than prices of imported steel (see Chart 1). Moreover, even if the prices of domestically- and foreign-sourced steel were the same, and the Department of Commerce’s measures of US productive capacity were fully reliable, US producers that rely heavily on imports of steel and aluminium would face sizeable short-run costs and disruptions.

Chart 1: Regional Comparison of Steel Prices

Source: “The Effect of Imports of Steel on the National Security,” An Investigation Conducted Under Section 232 of the Trade Expansion Act of 1962, as Amended, US Department of Commerce, January 11, 2018.

Effects on the economy and inflation. The tariffs would raise the costs of imported aluminium and steel. Assuming the supplies of US-sourced steel and aluminium are fairly inelastic in the short run, and incorporating disruptions and costs of transitions, business operating costs would rise and business production processes would be less efficient. Uncertainty will be added to business expansion plans. Certain industries, such as motor vehicles that are in the process of transforming the content of their products, will be disrupted.

In an environment of soft aggregate product demand, businesses would have little flexibility to raise product prices, and their margins would be squeezed. The impact on consumer prices and inflation would be minor. However, current macroeconomic conditions are favorable, and strengthening product demand would provide businesses flexibility to raise product prices. Nominal GDP, the broadest measure of current dollar spending and aggregate product demand, accelerated to 5 per cent in the second half of 2017, up from an average of 3.7 per cent in the prior five years, and that momentum is expected to be sustained. Accordingly, the effect of the higher tariffs would be shared by the real economy and inflation. While the effect on inflation would not be major, it would cut into real consumer purchasing power and add to price pressures at a time when markets are sensitive to inflationary expectations.

In response to the perceived negative effect of the tariffs — with the threats of retaliation in the headlines — the natural consequence is to put downward pressure on the US dollar. With a lag, this would raise prices of non-energy imports. Effectively, this would partially mitigate the effect of the tariffs on US multi-national firms but reduce the purchasing power of US consumers. The history of international trade policy shows that the nations that impose barriers to trade are hurt the most.

The initial negative response of the stock market reflects concerns about the momentum in the economy and profits.

We try to provide even-handed analysis, but these proposed tariffs may dent the current economic momentum. We have emphasized the very positive economic effects of the elevated business and consumer confidence and anticipate healthy responses to the Tax Cuts and Jobs Act. In this context, the proposed tariffs represent wrong-headed approaches to trade policy, in our view, and their timing is decidedly poor.

We believe the Trump Administration would be wise to reconsider and withdraw its proposal. If the goal is to meet domestic demand with domestically-produced steel or aluminum, pursuing this goal through constructive incentives such as improving tax policy, eliminating burdensome regulations, and providing incentives to improve efficiencies is a far better approach than punitive actions and penalties against international producers.

This article first appeared on E21. Read the original here.