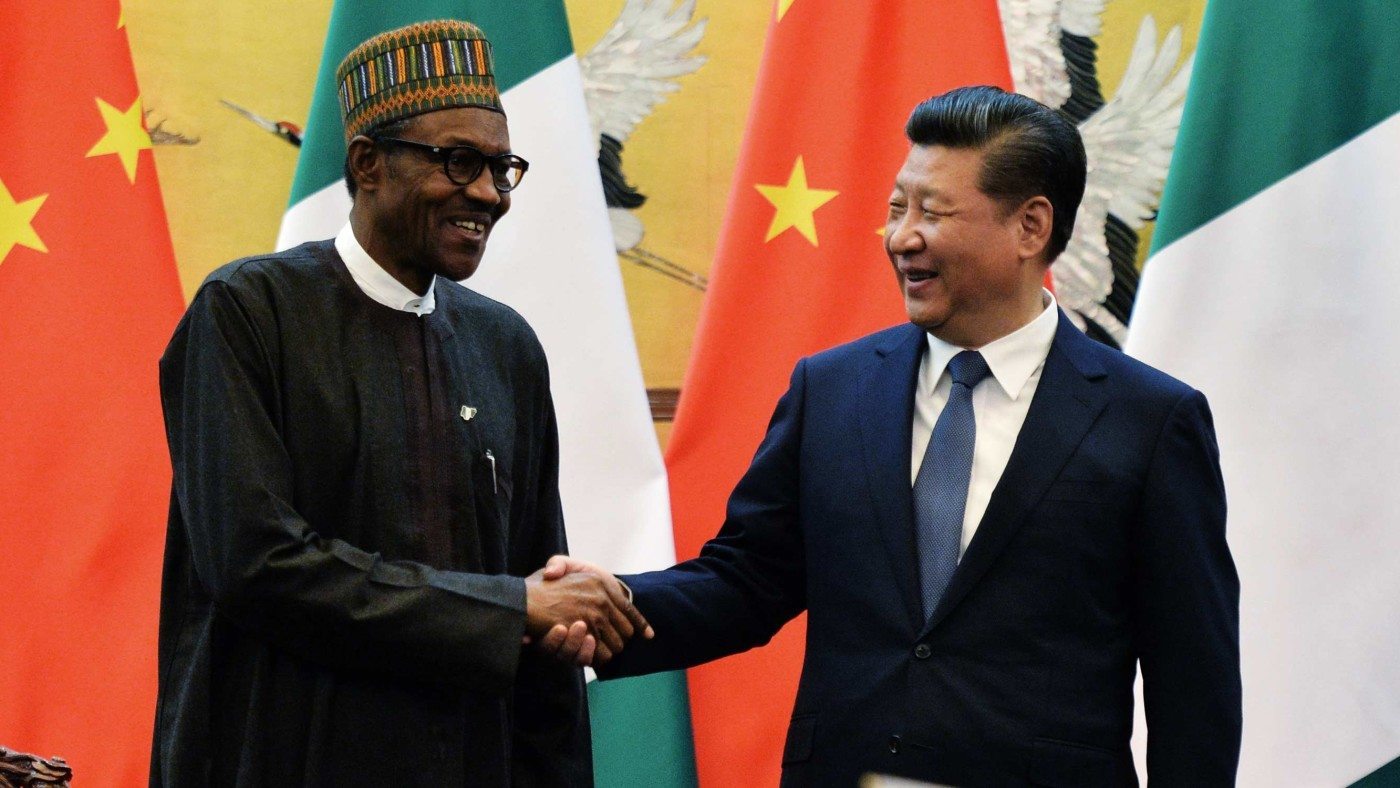

Nigeria’s Minister of Foreign Affairs, Mr. Geoffrey Onyema, announced on Tuesday that China has offered Nigeria a $6 billion loan to fund infrastructure projects. Onyema and President Muhammadu Buhari secured the deal with President Xi Jinping in Beijing, where Buhari is currently on his first official state visit to China at the invitation of the Chinese president.

The confirmation by Onyema coincided with an agreement reached between Nigeria and China yesterday on a currency swap deal, as he looks for ways to shore up the naira, Nigeria’s currency, and fund a record budget deficit.

Onyema announced that the credit would be:

“on the table as soon as we identify the projects. It won’t need an agreement to be signed; it is just to identify the projects and we access it.”

The loan comes at a good time as Nigeria faces its worst economic crisis in decades. The country’s projected 2016 deficit is currently at N2.2 trillion ($11.1 billion). Sinking oil prices have eaten into its foreign reserves and the naira has weakened against other currencies. As a resource-rich country, Nigeria’s economic performance has unfortunately been driven by the oil and gas sector. Unfortunate because the progress recorded towards genuine economic development prior to the discovery of oil in commercial quantity has since been virtually eroded. Relying on oil and gas for around 40% of GDP (50% at peak production in 2004) has left the economy vulnerable to the global oil price crash. The sector also represents 90% of their total exports.

But the oil crash cannot be blamed entirely – Nigeria’s quest for development has spanned decades not months. It is still yet to deliver on the ultimate goal of poverty reduction, despite various plans, programmes, and projects. There is also the added pressure from Buhari who plans to triple capital spending in the 2016 fiscal year.

Much like the despair felt worldwide for economic basket-case Zimbabwe, one can’t help but feel frustrated at the mismanagement of Nigeria’s abundant natural resources. In addition to oil and gas, Nigeria also boasts sizeable reserves of: tin, iron ore, coal, limestone, niobium, lead, zinc and arable land. Its rainforest region is also amongst the richest and most important in the continent for research and conservation. Yet as the World Bank said in 2007, weak and unreliable infrastructure, macroeconomic instability, microeconomic risks from corruption and weakness of institutions and regulations to guide investment behaviour are the main constraints to high performance of the economy.

China and Nigeria established a diplomatic tie in 1972 but the last decade has seen unprecedented developments in bilateral trade agreements, as well as business and diplomatic relations; trade volumes have risen from $2.8 billion in 2005 to $14.9 billion in 2015. Amongst the agreements signed, several so called Memoranda of Understanding (MOUs) have been included, supposedly indicative of the cordial relationship.

During Buhari’s current visit to Beijing, the Industrial and Commercial Bank of China Ltd (ICBC), the world’s biggest lender, and Nigeria’s central bank signed a deal on yuan transactions.

“It means that the renminbi (yuan) is free to flow among different banks in Nigeria, and the renminbi has been included in the foreign exchange reserves of Nigeria,” said Lin Songtian, Director General of the African Affairs Department of China’s foreign ministry. Nigeria has also been looking at Chinese panda bonds – a Chinese renminbi-denominated bond from a non-Chinese issuer, sold in the People’s Republic of China – on the justification that they would be cheaper than Eurobonds.

This move should not come as a shock to Europe. Nigeria converted up to a tenth of its reserves into yuan five years ago. A Mandate Letter Between the Industrial and Commercial Bank of China and the Central Bank of Nigeria on Renminbi (RMB) Transactions has also been signed.

Other examples of deepening ties have been hidden in plain sight. 46 million Yuan was gifted to Nigeria by China for the purpose of purchasing anti-malaria medicines and for training of Nigerian health personnel on malaria control. Whilst I support that latter move, unfortunately the Chinese government has also been training Nigerian doctors in the art of traditional Chinese medicine. Whatever the benefits of traditional Chinese medicine are, it cannot as yet cure malaria or HIV. There are 3,400,000 adults are currently living with HIV in Nigeria (that’s 9% of all people living with HIV globally) and there has been no reduction in annual fatalities caused by HIV since 2005. Perhaps widening access to antiretroviral treatments (only 20% of infected patients in Nigeria currently have access to treatment), improving administration of the drugs, and increasing education in schools about HIV transmission would be a more appropriate investment China could make to Nigeria’s health industry.

It is now emerging quite how thoroughly China has infiltrated the Nigerian state. From Beijing, Buhari has mandated that technical committees should be established immediately to finalise discussions on the new joint Nigeria/China rail, power, manufacturing, agriculture and solid mineral projects that have been agreed on. (The technical committees are to conclude their assignments before the end of next month.) There is also a $2 billion loan deal between ICBC and the Dangote Group, the company owned by Africa’s richest man (Aliko Dangote), to fund two cement plants it plans. Most alarmingly, Xi has responded to to Buhari’s desire to get the country self-sufficient in food production by offering an additional $15 million in agricultural assistance to Nigeria. The caveat is that 50 Agricultural Demonstration Farms would be established across the country, presumably run by Chinese management.

At the talks, Buhari has welcomed China’s readiness to assist Nigeria. What is not clear is whether his enthusiasm is because he genuinely believes this readiness to invest is part of some philanthropic mission to rapidly industrialise the African nation and help Nigeria join the world’s major economies, or because he desperately needs a major injection of cash into his economy and refuses to devalue the naira. The two Presidents do have a few similarities: namely, their public (but still largely ineffectual) wars on corruption, and their favouring of tax incentive programmes to attract business. But they are in no way equals in this relationship.

Buhari has warned Chinese investors not to see his country as a market for dumping goods:

“Although the Nigerian and Chinese business communities have recorded tremendous successes in bilateral trade, there is a large trade imbalance in favour of China, as Chinese exports represent some 80% of the total bilateral trade volume. This gap needs to be reduced. Therefore, I would like to challenge the business communities in both countries to work together to reduce the trade imbalance.”

Xi has said that China will support Nigeria playing a bigger role in international and regional affairs, and strengthen communication and coordination on major issues such as the peace and stability of Africa, climate change, and the 2030 Agenda for Sustainable Development. The first part shouldn’t be too hard. With Zuma steering South Africa into the rocks, Nigeria is comfortably Africa’s biggest economy. Zimbabwe is already a sure-fire trading partner, seeing as China also governs business there. And with China at the helm it looks as though the investments into aviation, technology, finance and mining will help patch up this looming $11.billion debt.

All in all, both men seem fairly pleased that China will help Nigeria solve the bottleneck of infrastructure, professionals and funds in developing industry and modern agriculture. Let’s hope the people of Nigeria pick up Mandarin quickly.